How Loya Insurance Claims Work After an Accident

For many drivers, the true test of an auto insurance company comes when they need to file a claim. Low premiums and flexible payments can help, but after an accident you need clear instructions, accurate documentation, and consistent follow-up.

Loya Insurance, also known as Fred Loya Insurance, provides a claims phone line at 1-800-880-0472 and tells customers to report a claim as soon as possible after an accident [1]. Understanding the process before you need it can reduce stress and help prevent avoidable delays.

If you are also trying to understand how accidents may affect future pricing, review how your driving record can affect insurance rates, auto insurance for first-time buyers, and Loya pay-as-you-go car insurance.

How to File a Claim With Loya Insurance

Loya tells customers to report a claim by calling 1-800-880-0472. The company’s claims page lists office hours from 8:00 a.m. to 7:00 p.m. MST Monday through Friday and 8:00 a.m. to 4:00 p.m. MST on Saturday [1]. Fred Loya’s contact page also lists the same claims phone number, plus 1-800-444-4040 for quotes and customer service [2].

Customers may also visit a local office or contact an agent for help, but the claims phone line is the most direct starting point. If you are filing against a Loya-insured driver rather than your own policy, the same claims department is generally the place to start.

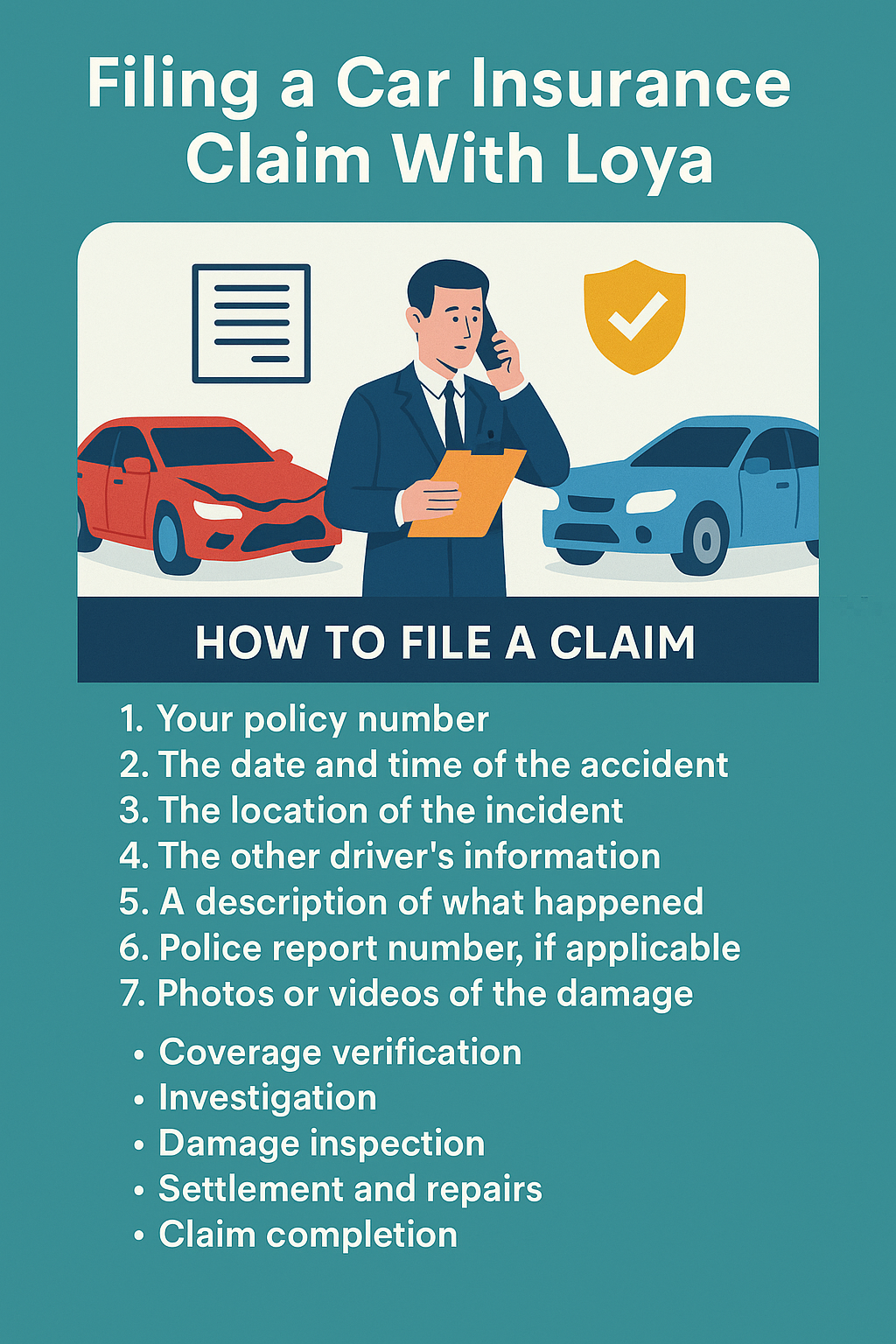

Call the claims line

Use the official claims number and have your policy number, accident date, location, and driver details ready.

Ask what is needed

Confirm which photos, reports, estimates, statements, and forms are required for your specific claim.

Track every contact

Write down the adjuster’s name, extension, claim number, date, time, and what was discussed.

What Information to Collect After an Accident

NAIC recommends exchanging information with the other driver after a crash, including name, address, insurance company name and phone number, driver’s license number, and license plate number if needed [3]. You should also collect photos, witness details, police report information, and a clear description of what happened.

| Information | Why it matters | How to document it |

|---|---|---|

| Your policy number | Helps the insurer locate your policy and verify coverage. | Save your ID card and declarations page in your phone. |

| Date, time, and location | Used to confirm the claim details and match reports or statements. | Write the exact location, nearby streets, weather, and traffic conditions. |

| Other driver information | Needed for liability investigation and communication with other insurers. | Take photos of insurance cards, license plates, and driver information when safe. |

| Photos and videos | Help document damage, vehicle positions, road conditions, and visible evidence. | Photograph all vehicles, plates, scene layout, skid marks, signs, and damage angles. |

| Police report details | May support the claim investigation and help establish basic facts. | Ask for the report number, officer name, and agency contact information. |

| Witness information | Can help if fault is disputed. | Collect names, phone numbers, and short notes about what each person saw. |

What Happens After You File a Claim

After you report the claim, Loya typically assigns the case to a claims adjuster. The adjuster reviews coverage, investigates the accident, requests documents, communicates with involved parties, and determines what the policy may pay based on coverage and liability.

III explains that insurers may require proof of claim forms and police report copies, and recommends asking about claim timing, required documents, and deadlines [4]. This is especially important if you have a liability-only policy, a deductible, disputed fault, or a financed vehicle.

Report

Call or contact the claims department and open the claim file.

Verify

The insurer checks whether the policy was active and what coverage applies.

Investigate

The adjuster reviews statements, photos, reports, and liability facts.

Estimate

Damage is inspected through photos, an adjuster, or repair estimate.

Resolve

The claim is paid, denied, repaired, settled, or closed based on the file.

What Loya Insurance Covers in a Claim

Coverage depends on the policy you purchased, the state where the policy applies, policy limits, deductibles, exclusions, and whether coverage was active at the time of the accident.

A liability-only policy usually focuses on damage or injuries you cause to others. It does not normally repair your own vehicle after an at-fault accident. Full coverage usually means collision and comprehensive are included, but deductibles and exclusions still apply.

Liability-Only vs. Full Coverage Claims

One of the biggest sources of claims frustration is misunderstanding what the policy actually covers. Before you file, review your declarations page and confirm whether you have liability-only, collision, comprehensive, uninsured motorist, medical payments, PIP, rental reimbursement, or roadside assistance.

| Coverage type | What it may cover | What to confirm |

|---|---|---|

| Liability-only | Damage or injuries you cause to others, up to your limits. | It usually does not cover your own car repairs after an at-fault accident. |

| Collision | Damage to your vehicle after a covered crash. | Your deductible, repair process, and whether the vehicle may be declared a total loss. |

| Comprehensive | Theft, vandalism, fire, hail, falling objects, and certain non-collision losses. | Your deductible, required documentation, and exclusions. |

| UM/UIM | May help when another driver has no insurance or not enough insurance. | Availability, state rules, limits, and whether injury or property damage applies. |

| Medical payments or PIP | May help with medical bills depending on your state and policy. | Required documents, deadlines, and coordination with health insurance. |

For related coverage help, review Loya non-owner car insurance and uninsured motorist coverage claim basics.

How Long Loya Claims May Take

Claim timelines vary based on the type of accident, the availability of documents, whether fault is disputed, whether injuries are involved, whether a police report is available, and how quickly each person responds. A simple claim may move faster, while disputed liability, missing documents, total losses, or multiple insurers can extend the process.

Fastest claims usually have…

- Active coverage confirmed quickly.

- Clear photos and police report details.

- No dispute about fault.

- Quick response to adjuster requests.

Claims slow down when…

- Documents are missing.

- Drivers disagree about fault.

- Injuries are involved.

- Vehicle value or repair estimates are disputed.

You can help by…

- Responding the same day when possible.

- Keeping organized notes.

- Saving every email and document.

- Confirming next steps after each call.

Common Loya Claims Challenges and How to Reduce Them

Budget-focused insurers can sometimes have less automated claims tools than large national carriers. That does not mean the claim cannot be handled properly, but it does mean policyholders should stay organized and proactive.

| Potential challenge | Why it happens | What you can do |

|---|---|---|

| Communication delays | Adjusters may be handling many files, or documents may still be pending. | Ask for the adjuster’s direct extension, send follow-up emails, and keep call notes. |

| Extra document requests | The insurer may need photos, statements, estimates, police reports, or proof of ownership. | Ask for a complete document list on the first call and submit everything together. |

| Fault disputes | The other driver may tell a different version of events. | Provide photos, witness names, dashcam footage if available, and police report details. |

| Coverage confusion | Liability-only customers may expect repairs to their own car to be covered. | Review the declarations page and ask which coverage applies before authorizing repairs. |

| Total loss value disagreement | Older or high-mileage vehicles may be valued differently than the owner expects. | Ask for the valuation report and provide comparable listings or repair records if relevant. |

How to Speed Up a Loya Insurance Claim

You cannot control every part of the claim, but you can reduce avoidable delays by staying organized and responding quickly. NAIC notes that a claims adjuster or repair shop may examine the damage and that the insurer uses the adjuster’s findings as part of the settlement process [5].

Do this immediately

- Report the claim as soon as possible.

- Send photos, videos, and police report details.

- Provide a clear statement of what happened.

- Ask whether a repair estimate or inspection is needed.

- Confirm whether rental or towing is covered.

Track everything

- Claim number.

- Adjuster name and extension.

- Date and time of each call.

- Documents sent and when.

- Next promised step.

- Settlement or denial explanation.

What to Do if Loya Denies Your Claim

If Loya denies your claim, ask for the denial explanation in writing. A written explanation should identify the reason for denial, such as inactive coverage, excluded driver, late payment, lack of applicable coverage, policy exclusion, misrepresentation, or another specific issue.

Common denial reasons

- The policy was not active on the accident date.

- The driver was excluded or not covered.

- The damage was not covered by the policy type.

- The claim involved business or delivery use not covered by the policy.

- The damage was pre-existing or not related to the accident.

How to respond

- Request the denial letter.

- Review your policy and declarations page.

- Ask for supervisor review if facts are wrong.

- Submit missing documents or corrected information.

- Contact your state insurance department if you need regulatory guidance.

What Happens When Another Driver Files a Claim Against You

If someone else files a claim against your Loya policy, cooperate with the adjuster. Provide your statement, photos, witness details, and any evidence that supports your version of events. If you do not respond, the insurer may have to rely more heavily on the other driver’s account and available documents.

Be factual and avoid guessing. If you are unsure about a detail, say that you are unsure. Do not admit fault at the scene or promise payment. Let the insurer investigate liability based on policy terms, statements, photos, police reports, and other evidence.

FAQ: Loya Insurance Claims

What is the Loya Insurance claims phone number?

Fred Loya lists 1-800-880-0472 as the number to file a claim. The company also lists 1-800-444-4040 for quotes and customer service.

When should I file a Loya claim?

File as soon as possible after an accident or covered loss. Waiting can make it harder to document the scene, reach witnesses, or meet policy deadlines.

Does liability-only coverage repair my own car?

Usually no. Liability-only coverage generally pays for damage or injuries you cause to others, up to policy limits. Your own vehicle normally needs collision or comprehensive coverage to be repaired under your policy.

What documents should I send after filing?

Common documents include photos, police report details, driver and insurance information, witness details, repair estimates, proof of ownership, and any forms requested by the adjuster.

Why is my Loya claim delayed?

Delays may happen because of missing documents, disputed fault, late responses, injury claims, repair shop delays, police report timing, or coverage questions.

Can I challenge a Loya claim denial?

You can request the denial in writing, review the reason, submit missing or corrected documents, ask for supervisor review, and contact your state insurance department if you need help understanding your rights.

The Final Word on Loya Insurance Claims

Loya Insurance claims are easier to manage when customers understand the process before an accident happens. Report the claim quickly, provide complete information, understand your coverage type, and stay organized during every conversation with the adjuster.

While Loya may not offer the same digital claims experience as some large national insurers, a well-documented claim can still move more smoothly. Keep records, respond promptly, ask what is needed next, and confirm how your policy limits and deductibles apply before making repair or settlement decisions.

References

- Fred Loya Insurance, File an Auto Insurance Claim with Fred Loya Insurance, including claim phone number and claim reporting guidance. Source↩

- Fred Loya Insurance, Contact page, including claims, customer service, and roadside assistance contact information. Source↩

- National Association of Insurance Commissioners, What You Should Know About Filing an Auto Claim, including information to collect after a crash. Source↩

- Insurance Information Institute, How to file an auto insurance claim, including documents and timing questions to ask. Source↩

- National Association of Insurance Commissioners, Don’t Be a Crash Dummy, including claim investigation and adjuster information. Source↩