Caught Driving Without Insurance: What Happens and What to Do Next

Driving without insurance can turn a simple traffic stop, accident report, or registration issue into a much bigger legal and financial problem. If you were caught driving uninsured, or you are worried because your policy has lapsed, the safest next step is to understand the consequences and get back into legal coverage as quickly as possible.

Most states require drivers to carry auto insurance or another approved form of financial responsibility. Uninsured driver rates also remain high enough that the issue affects everyone on the road, not only the driver who skipped coverage [1]. The good news is that many drivers can still compare lower-cost options, restart coverage, and avoid making the situation worse.

If cost is the reason you are uninsured, start by reviewing car insurance basics, the consequences of driving uninsured, and how to compare auto insurance quotes.

Quick Take

The key is not whether you can “get away with it.” The key is how quickly you can fix the coverage problem.

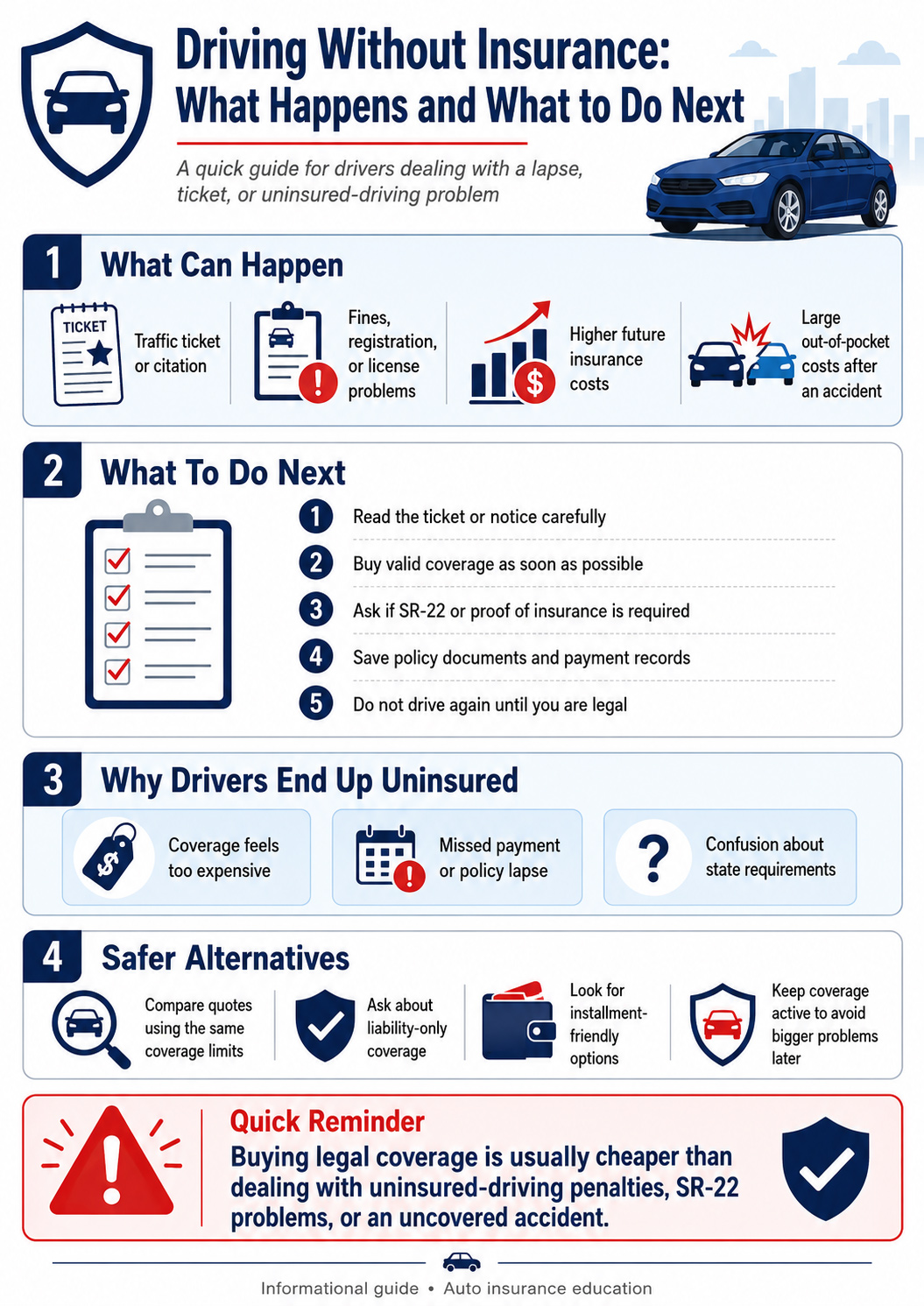

- Driving uninsured can lead to fines, registration issues, license problems, and higher future premiums.

- An accident while uninsured can create large out-of-pocket costs.

- Some drivers may need SR-22 or proof-of-insurance filings after a violation.

- Buying legal coverage is usually cheaper than dealing with penalties after being caught.

Legal Risk

In many states, driving without required coverage can lead to citations, fines, proof-of-insurance requirements, and registration or license complications. Even where rules differ, the financial exposure remains serious [2].

Financial Risk

If you cause a crash, there may be no insurer stepping in for you. Repairs, medical bills, towing, lost wages, and legal claims can become your responsibility.

Future Insurance Risk

A coverage lapse or uninsured-driving violation can make future insurance harder or more expensive to obtain, especially if an SR-22 filing becomes required.

What Happens If You Are Caught Driving Without Insurance?

The exact penalty depends on the state, your driving history, whether you were involved in an accident, and whether this is a first offense. But the common pattern is simple: the longer the problem goes unresolved, the more expensive and complicated it can become.

Proof of insurance may be requested during a traffic stop, after a crash, during registration renewal, or through a state insurance verification system. In California, for example, insurance is required on vehicles operated or parked on public roads [3]. Other states have their own rules, but the core risk is similar: if you drive without required coverage, you may face penalties and financial exposure.

| Situation | What Can Happen | Why It Matters |

|---|---|---|

| Routine traffic stop | An officer may request proof of insurance and issue a citation if you cannot provide it. | A small stop can become a costly legal and administrative problem. |

| Accident while uninsured | Police reports, civil liability, towing bills, vehicle damage, and injury claims may follow. | This is often when driving uninsured becomes far more expensive than the premium you skipped. |

| Registration or DMV issue | Proof of financial responsibility may be required, and missing coverage can trigger suspension or reinstatement steps. | Your ability to drive legally may be affected until you fix the issue. |

| Future insurance shopping | Insurers may treat you as higher risk because of a lapse, violation, or SR-22 requirement. | You may pay more later even if you are trying to buy affordable coverage again. |

What To Do If You Were Caught Driving Without Insurance

If you already received a ticket, notice, or accident report, do not ignore it. The right response depends on your state and situation, but these steps can help you limit further problems.

Important: This is general information, not legal advice. If you received a citation, were involved in an accident, or have a suspended license, review the official notice and contact your state DMV, insurer, or a qualified attorney for case-specific guidance.

- Read the citation or notice carefully. Look for deadlines, court dates, proof-of-insurance instructions, reinstatement steps, and payment requirements.

- Buy valid coverage as soon as possible. A new policy may not erase the violation, but it can help you stop the problem from getting worse.

- Ask whether proof of insurance or SR-22 is required. Some drivers need to file proof of financial responsibility after an uninsured-driving violation or suspension.

- Keep records of everything. Save policy documents, ID cards, payment receipts, DMV letters, and court paperwork.

- Do not drive again until you know you are legal. If your license or registration is suspended, coverage alone may not be enough; you may need formal reinstatement.

- Compare quotes before renewing blindly. Once coverage is active, compare options again so you can keep a policy you can afford.

Why Some Drivers End Up Uninsured

Many drivers do not go uninsured because they want to break the rules. Often, the issue starts with affordability, a missed payment, a billing problem, a cancelled policy, a move, or a misunderstanding about state requirements. That does not remove the risk, but it does mean the solution should be practical.

If coverage feels too expensive, the better move is to shop strategically instead of driving bare. Start with liability-only quotes, compare the same coverage limits across companies, ask about installment options, and review choices designed for non-standard or higher-risk drivers.

Reason #1: “I barely drive.”

Low mileage may reduce how risky driving feels, but one uninsured accident can still produce large out-of-pocket losses.

Reason #2: “Insurance costs too much.”

That is a real concern, but there are usually cheaper legal options before going uninsured, especially if you compare multiple quotes.

Reason #3: “My policy just lapsed.”

A short lapse can create long-term pricing problems. Restarting coverage quickly is usually better than waiting until you are stopped or involved in a crash.

What To Do Instead If Coverage Feels Unaffordable

- Compare several quotes using the same coverage limits. This gives you a fair comparison instead of mixing cheap but weak policies with stronger ones.

- Ask whether liability-only coverage fits your situation. For an older vehicle, full coverage may not always be the most cost-effective choice.

- Look for installment-friendly options. Monthly payment flexibility can be more realistic than a large upfront bill.

- Review discounts carefully. Multi-car, homeowner, prior-insurance, paperless, and defensive driving discounts may help.

- Keep your coverage active. A lapse in insurance can make future quotes worse.

- Consider uninsured/underinsured motorist protection. This may help if someone else hits you and they do not have enough coverage [1].

Smarter Questions To Ask Before You Drive Again

- What is the legal minimum in my state? Start there, but remember that the minimum may not be enough to protect your finances after a serious crash.

- Is my license or registration currently valid? If either one is suspended, buying insurance may be only one part of the fix.

- Do I need SR-22 or proof of financial responsibility? If your notice mentions SR-22, ask the insurer if it can file it in your state.

- How much would one at-fault accident cost me out of pocket? Repairs, medical bills, rental car costs, and lost income can stack up fast.

- Would a short lapse cost me more later? In many cases, yes. Continuous coverage can matter when insurers price your next policy.

- Am I protected if someone uninsured hits me? If not, review our guide to uninsured vs. underinsured motorist coverage.

When You May Need SR-22 After Driving Uninsured

Some drivers who are caught without insurance may be required to file SR-22 or another proof-of-financial-responsibility document. This depends on the state, the violation, and whether there was an accident, suspension, or repeat offense.

An SR-22 is not a separate insurance policy. It is a certificate filed by an insurance company to show the state that required coverage is active. If you are told you need one, read our guide to Loya SR-22 insurance and our checklist for cheap SR-22 insurance from Loya.

If You Own a Car

You may need a regular auto policy with the required filing attached to it.

If You Do Not Own a Car

You may need to ask about non-owner insurance if the state still requires proof of financial responsibility.

If You Had a Lapse

Restart coverage quickly and avoid another cancellation during any required monitoring period.

Driving Without Insurance FAQs

Can you drive without insurance if you are careful?

No. Being careful does not remove the legal requirement to carry insurance or proof of financial responsibility where required. It also does not protect you from the cost of an accident.

What happens if you get pulled over without insurance?

The result depends on your state and driving history, but you may face a citation, fines, proof-of-insurance requirements, registration issues, license problems, or higher future premiums.

Can you get insurance after being caught without it?

Yes, many drivers can still buy coverage after a lapse or violation. The price may be higher, and some drivers may need SR-22 or proof-of-financial-responsibility filing.

Is driving uninsured cheaper than buying coverage?

Usually no. It may feel cheaper in the short term, but one ticket, lapse penalty, registration issue, or uninsured accident can cost far more than maintaining basic coverage.

Should I drive while waiting for a new policy?

No. Wait until coverage is active and you have proof of insurance. If your license or registration was suspended, confirm that you are legally reinstated before driving.

Bottom Line

Trying to avoid getting caught without insurance is the wrong goal. The better goal is to get legal, affordable coverage in place and avoid a lapse that can make your future premiums worse. With uninsured-driver rates still significant nationwide, the need for proper coverage is not theoretical. It affects real accidents, real households, and real budgets every day [1].

If price is the problem, compare quotes, simplify coverage where appropriate, and choose a plan you can realistically keep active. That approach is safer, smarter, and usually cheaper than paying fines, handling repairs alone, or facing liability after a crash.