If you live in the Southwest or in a state where Loya Insurance operates, you may have seen ads for low-cost auto insurance, flexible payments, and help for drivers who need coverage quickly. For drivers who have been quoted high rates, canceled, or required to carry an SR-22, cheap Loya car insurance can look like a practical way to get back on the road.

Still, the lowest monthly payment is not always the best policy. NAIC explains that auto policies can include liability, medical payments, uninsured/underinsured motorist coverage, and coverage for damage to your auto, so shoppers should understand what is included before choosing a policy [1].

Use this guide to understand how Loya can fit into a budget-focused insurance plan, what tradeoffs to watch, and how to compare a cheap quote without giving up protection you may need.

Drivers who need affordable coverage, flexible payments, or help after a lapse.

Liability limits, fees, deductibles, exclusions, and claim rules.

SR-22 filing, UM/UIM, payment fees, down payment, and policy term.

Compare total policy cost, not only the first payment.

Quick summary: Loya can be useful for budget-focused or higher-risk drivers, but a cheap policy only works if the limits, deductibles, and coverage types match your real risk. Before buying, compare the total cost for the policy term, confirm whether fees apply, and make sure the quote includes the coverage you actually want.

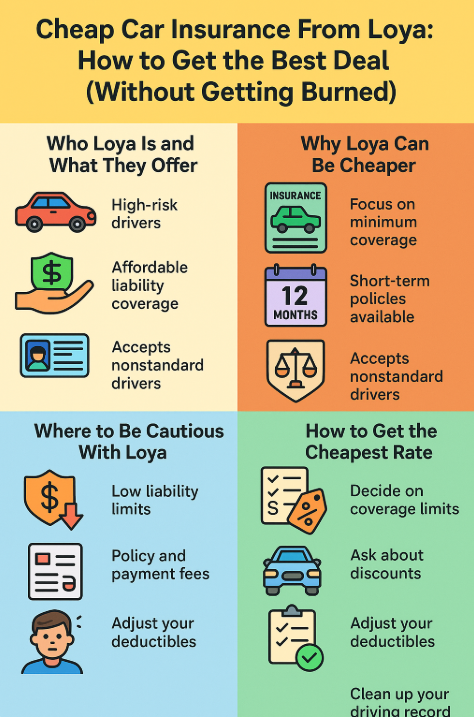

Who Loya Insurance Is and What They Offer

Loya Insurance is known for affordable auto insurance options, local offices, bilingual support in many areas, cash-payment convenience, and help for drivers who may not fit neatly into a preferred-risk profile. Many shoppers look at Loya after a lapse, accident, ticket, SR-22 requirement, or high quote from another insurer.

Loya policies may include standard auto insurance coverage categories such as liability coverage, comprehensive and collision for physical damage, uninsured/underinsured motorist coverage where available, medical payments or PIP depending on state rules, and SR-22 filings for drivers who need proof of financial responsibility.

If you want a deeper breakdown of available coverage categories, review Loya auto insurance coverages. If you need a filing after a suspension or serious violation, compare options with Loya SR-22 insurance.

Budget-Focused Drivers

Loya may appeal to drivers who need legal coverage quickly and want flexible payment options.

Nonstandard Situations

Drivers with tickets, accidents, lapses, or SR-22 needs may compare Loya when preferred carriers are expensive.

Local Support

Some shoppers prefer local office service instead of managing everything through an app or call center.

Why Loya Can Look Cheaper Than Larger Competitors

Loya can look cheaper in some comparisons because many shoppers are buying basic liability or state-minimum coverage rather than high-limit policies with every optional add-on. A minimum-coverage policy naturally costs less than a policy with higher liability limits, collision, comprehensive, rental reimbursement, roadside assistance, and other extras.

Another reason is market focus. Some national insurers price higher-risk drivers aggressively or may not want certain risk profiles. If Loya is more willing to quote drivers with prior lapses, violations, or SR-22 needs, it may offer a more realistic option for those drivers.

| Why a Quote Looks Cheap | What It Means | What to Check |

|---|---|---|

| Minimum liability limits | The policy may meet state law but provide limited financial protection. | Compare higher limits before choosing the lowest option. |

| No full coverage | The quote may not include collision or comprehensive for your own car. | Confirm whether your vehicle would be repaired after a covered crash or theft. |

| Higher deductibles | The premium can drop, but you pay more after a covered claim. | Choose a deductible you could pay quickly. |

| Short-term payment focus | The first payment may look low, while fees raise the total cost. | Ask for the total cost for the entire policy term. |

The Hidden Risks Behind Very Cheap Auto Insurance

The biggest risk with any cheap auto insurance policy is underinsuring yourself. State minimum liability may keep you legal, but it may not be enough after a serious crash. If you cause more damage than your policy covers, the extra cost can become your personal responsibility.

Uninsured driver risk is also real. NAIC reports that 15.4% of motorists were uninsured in 2023, and uninsured motorist rates varied widely by state [2]. That is why uninsured/underinsured motorist coverage can matter even when you are shopping for a low price.

How Much Liability Coverage Should You Consider?

Every state sets its own minimum requirements, but the minimum is not automatically the best choice. A low-limit policy can be useful when money is tight, but serious crashes can exceed minimum limits quickly. The better approach is to compare more than one limit level before deciding.

Minimum Coverage May Fit If

- You need the lowest legal price right now.

- Your vehicle is older and paid off.

- You understand that your own car may not be covered.

- You plan to upgrade later when your budget improves.

Higher Limits May Fit If

- You have income, savings, or assets to protect.

- You drive often or commute in heavy traffic.

- You live in a state with expensive repair or medical costs.

- You want more protection against lawsuits after a serious accident.

If you are comparing coverage choices, this guide on Loya insurance deductibles can help you understand how deductible decisions affect price and claim-time costs.

Fees, Down Payments, and Monthly Payments

A policy can look cheap because the first payment is low, but the true cost depends on the full term. Some low-cost and nonstandard policies may include policy fees, installment fees, reinstatement fees, late fees, or other charges. Those small charges can add up across six or twelve months.

| Cost Item | Why It Matters | Question to Ask |

|---|---|---|

| Down payment | A low down payment can help you start coverage, but it may not mean the total policy is cheaper. | What is the total cost for the full term? |

| Installment fees | Monthly payments may include added fees. | How much more do I pay if I choose monthly payments? |

| Late fees | Missing payment dates can increase cost or risk cancellation. | Is there a grace period, and what happens if payment is late? |

| Reinstatement fees | If coverage lapses, getting it active again may cost extra. | What fees apply if my policy cancels for nonpayment? |

SR-22 Drivers: Why Loya May Be Worth Comparing

Drivers who need an SR-22 often face higher prices because the filing is usually tied to a serious violation, suspension, or proof-of-insurance requirement. Fred Loya’s SR-22 page says agents can help with an SR-22 certificate and customized auto insurance policy based on state minimum requirements and coverage options [3].

If you are required to carry an SR-22, continuous coverage matters. A lapse can create more problems with your license or state filing. When comparing policies, ask whether the SR-22 filing is included, how quickly it is filed, and what happens if the policy cancels.

Ask About Filing

Confirm whether the insurer files electronically, what the filing fee is, and how long it takes.

Avoid Lapses

Make every payment on time. A lapse can trigger state notification and create license problems.

Re-Shop Later

As violations age and requirements end, compare again to see whether better rates are available.

Discounts and Money-Saving Moves With Loya

Even when shopping with a budget carrier, you should still ask about discounts and pricing levers. The easiest mistake is accepting the first low quote without asking whether there is another safe way to reduce the total cost.

Possible Savings Questions

- Do I save by paying in full?

- Can I add multiple vehicles?

- Does prior insurance help?

- Are paperless, autopay, or renewal savings available?

- Can a higher deductible reduce my full-coverage premium?

Do Not Cut These Blindly

- Bodily injury liability.

- Property damage liability.

- Uninsured/underinsured motorist coverage.

- Collision and comprehensive on financed cars.

- Coverage required by your lender or state.

For more savings ideas, review top car insurance discounts for young drivers. Some discount categories can still help other drivers understand what insurers may consider.

Loya vs. Mainstream Insurers: Price vs. Value

Loya may be strongest when you need affordable coverage quickly, prefer in-person service, need flexible payment options, or have a driving history that makes other insurers expensive. But a fair comparison should look beyond the monthly payment.

Mainstream insurers may sometimes offer better value for drivers with improving records, continuous coverage, higher limits, or multiple-policy needs. A slightly higher monthly premium can be worthwhile if the total term cost is similar and the policy includes better limits, fewer fees, stronger service, or more digital convenience.

| Compare | Loya May Help If | Another Insurer May Help If |

|---|---|---|

| Driving record | You have tickets, accidents, lapses, or SR-22 needs. | Your record is clean or improving. |

| Payment style | You need a low start-up cost or local payment option. | You can pay in full or want autopay/paperless tools. |

| Coverage level | You mainly need basic legal coverage. | You want higher limits, full coverage, or bundled options. |

| Long-term value | You need coverage now while rebuilding your profile. | You want broader service, policy features, or lower total term fees. |

A Step-by-Step Plan to Shop Loya the Smart Way

The best way to shop Loya is to decide your coverage floor before you ask for the cheapest quote. That way, you can pursue savings without accidentally buying a policy that does not match your needs.

- Gather your details. Have driver’s license information, VINs, estimated mileage, current declarations page, and any SR-22 requirement ready.

- Set your minimum limits. Decide your liability limits, deductible, UM/UIM preference, and whether you need collision and comprehensive.

- Ask for a full cost breakdown. Request the down payment, monthly payment, fees, total term cost, and cancellation terms.

- Compare equal coverage. Get quotes from several insurers using the same limits and deductibles.

- Review every 6 to 12 months. Re-shop when tickets age, your SR-22 period changes, your credit improves where allowed, or your coverage needs change.

Using Loya as a Stepping-Stone

For some drivers, Loya may be a short-term stepping-stone rather than a permanent insurance solution. If your record is rough, your coverage lapsed, or you need an SR-22, getting affordable coverage active can be valuable. Then you can use the next year or two to improve your record, avoid tickets, keep coverage continuous, and compare again later.

During that time, keep strong records. Save payment receipts, policy declarations, ID cards, claim documents, and confirmation of any SR-22 filing. If you pay in cash or in person, documentation can help prevent confusion later.

If you are ready to compare coverage, use how to get a Loya car insurance quote as a starting point. If you ever need claims help, Fred Loya’s claims page says customers can report a claim at 1-800-880-0472 [4].

The Final Word on Cheap Car Insurance From Loya

Cheap car insurance from Loya can be a practical option when you need affordable coverage, flexible payments, or help after a lapse, ticket, accident, or SR-22 requirement. The key is to avoid buying only on the lowest first payment.

Decide your coverage needs first, compare total policy cost, ask about all fees, confirm whether the quote includes UM/UIM or full coverage where needed, and re-shop regularly as your profile improves. When you approach Loya with a clear plan, you can use the potential savings without exposing yourself to unnecessary financial risk.